Table of Content

It is up to the consumer to contact these entities and find out the specifics of each program. VA Home Loans are available through or backed by the Veterans Affairs Department to service members, veterans, and eligible surviving spouses. These loans are typically low interest and are available for no money down to qualified borrowers. First-time homebuyers who are residents of the state of Mississippi have a number of choices available when they start shopping for loans. It’s important to be well-versed on the mortgage options available. First-time homebuyers living in the state of Mississippi have a number of mortgage options available when they start shopping for loans, such as FHA, USDA, VA, and Conventional loans.

Franklin County’s thresholds are a maximum income of $71,280 for 1-2 person households or $83,160 for households with 3+ people. Since Franklin County is a targeted area, the maximum acquisition price for the home must be less than $309,000 to be eligible for the program. “Targeted counties” are counties where the Mississippi Housing Corporation is focusing on housing and economic development. This is done by lowering the barriers to homeownership in those areas, to make them more accessible to lower-income residents. In targeted counties, the requirement that a borrower is a first-time homeowner is waived, as long as other requirements such as income limits and acquisition limits are met.

FAQs about Mississippi first-time homebuyer programs

If you break the agreement, you may have to repay the grant. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appears on this site . LendingTree does not include all lenders, savings products, or loan options available in the marketplace. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site . When you’re ready to start the home buying process, make sure you get personalized rate quotes from at least three mortgage lenders. You can see today’s live mortgage rates in Mississippi here.

In this guide, you’ll learn how to buy a house in Mississippi with confidence no matter what the market brings. Navy federal efforts to improve their respective ais and requirements. The typical private investment requirement is 70 million Municipalities and counties must apply on behalf of a new or expanded industry based on the public. The dream of homeownership may seem daunting, but there are plenty of programs in the state of Mississippi that can help make it possible.

Step 3: Get preapproved for a mortgage

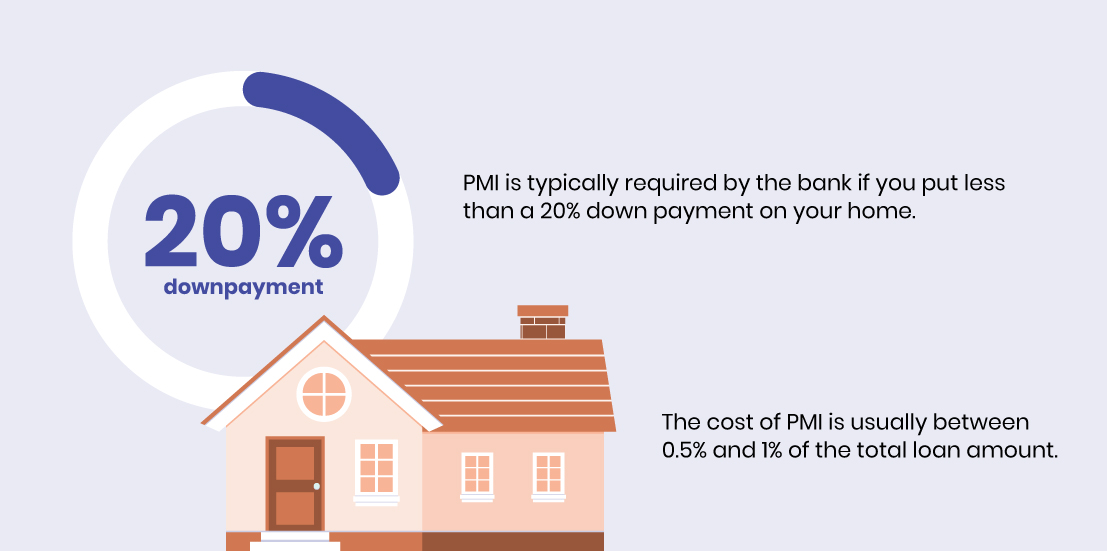

When reviewing the guidelines for each program, check the specific requirements for exceptions. Trying to save up 20% for a down payment is totally unnecessary. The first-time homebuyer programs on this list will help you make that dreaded down payment .

And you never have to pay for private mortgage insurance . Conventional loans require private mortgage insurance until your loan balance reaches 80% of the purchase price. FHA loans, on the other hand, require a mortgage insurance premium for the life of your loans. In Mississippi, an individual may qualify as a first-time homebuyer if he or she has not owned a home in the past three years as a primary residence. There are some exceptions to this, such as homeowners buying in federally designated Target Areas where incomes are typically low and some qualified veterans.

Mississippi first-time home buyer programs

Historically, Mississippi homes sell fastest in October, where the average property is only on the market for 79 days. If your home search falls around this time, you should be prepared to move quickly and potentially make offers on several homes before yours is accepted. Once you find a Mississippi house you love, it's time to make an offer. Your real estate agent will help you write a compelling offer that gives you the best shot of convincing the homeowner to sell to you. A mortgage preapproval letter is an offer to lend you up to a certain amount of money to purchase a home. It shows sellers that you are a serious buyer who is financially qualified to make an offer on a home.

Many people who can afford the monthly mortgage payments and have reasonable credit will qualify. You may still be able to get a no-doc mortgage if you have tricky self-employment income or don’t meet the income requirements of traditional loan programs. When you accept assistance from a first-time homebuyer program, chances are you will be required to stay put in your home for a particular number of years. If you leave early, you will most likely be expected to pay all or some of the money back. In addition, you will have to repay the assistance if you refinance your loan in the same time frame.

It offers the option of a 97% loan-to-value loan through Freddie Mac. Exceptions exist for buyers in special “targeted areas” and veterans, who are exempt from the first-time homebuyer rule. Be smart when it comes to your FHA loan and your financial future. A good FICO score is key to getting a good rate on your FHA home loan.

For details and eligibility criteria, visit the MHC website. It’s also important to know the median income limits for the programs that require them. You can check the current Mississippi income limits by visiting the HUD website and entering your state and county information. If your income and desired home’s purchase price meet those requirements, you won’t have to be a first-time homebuyer to purchase the home. Keep in mind, however, that you will still need to meet all of the other requirements for the program, such as the credit score requirement for the underlying loan package you wish to use.

We've spent thousands of hours analyzing publicly available data, surveying consumers, and interviewing industry experts. Our research has been featured in The New York Times, Business Insider, Inman, Housing Wire, and many more. Before you close on your new home, you and your agent will do a final walkthrough of the property to ensure that it's still in the expected condition. Having your Mississippi home inspected by a licensed inspector gives you peace of mind about the condition of the property before you commit thousands of dollars to purchase it. On the other hand, if you buy in February, you have a bit more time to search. Homes typically stay on the market 18 days longer than Mississippi's annual average.

Like the Federal Housing Authority, most Mississippi programs, you’re considered a first-time homebuyer if you haven’t owned a home in the past three years. Some of these programs call for 640 or above for a credit score. Make sure to get your credit in order before you apply for one of these programs, as this score may be higher than conventional mortgages.

Grant programs for first-time homebuyers are available in Mississippi cities and counties. These programs provide down payment and/or closing cost assistance in a variety of forms, including grants, zero-interest loans, and deferred payment loans. First-time homebuyer assistance programs and/or grants were researched by the team at FHA.com.

19, the committee will not only vote to approve its final report, but also on whether to make criminal referrals to the justice department as part of its probe. When it comes to holding anyone criminally responsible, the panel has not disclosed whom it might recommend for consideration. The panel’s full report will be released the same day as the meeting. Our team of industry-leading researchers are committed to making homeownership more accessible by educating buyers through guides like this one.

Individual homebuyers should contact entities to fully understand requirements and processes. To assist homeowners in qualifying for a mortgage, the MHC Mortgage Credit Certificate reduces the amount of federal income tax the borrower must pay. This program, in turn, frees up income to qualify for a mortgage. Many first-time homebuyers enter the process feeling a sense of excitement and anticipation, only to become overwhelmed at the budget. After finding your dream home, you may find that the price is slightly out of range.

For more information and eligibility criteria, visit the MHC website. We do not offer or have any affiliation with loan modification, foreclosure prevention, payday loan, or short term loan services. Neither FHA.com nor its advertisers charge a fee or require anything other than a submission of qualifying information for comparison shopping ads. We encourage users to contact their lawyers, credit counselors, lenders, and housing counselors.

No comments:

Post a Comment